The digital world is changing rapidly. Traditional systems of storing and verifying information are being challenged by new technologies that promise transparency, security, and decentralization. Among these innovations, Blockchain has emerged as one of the most influential technologies of the modern era.

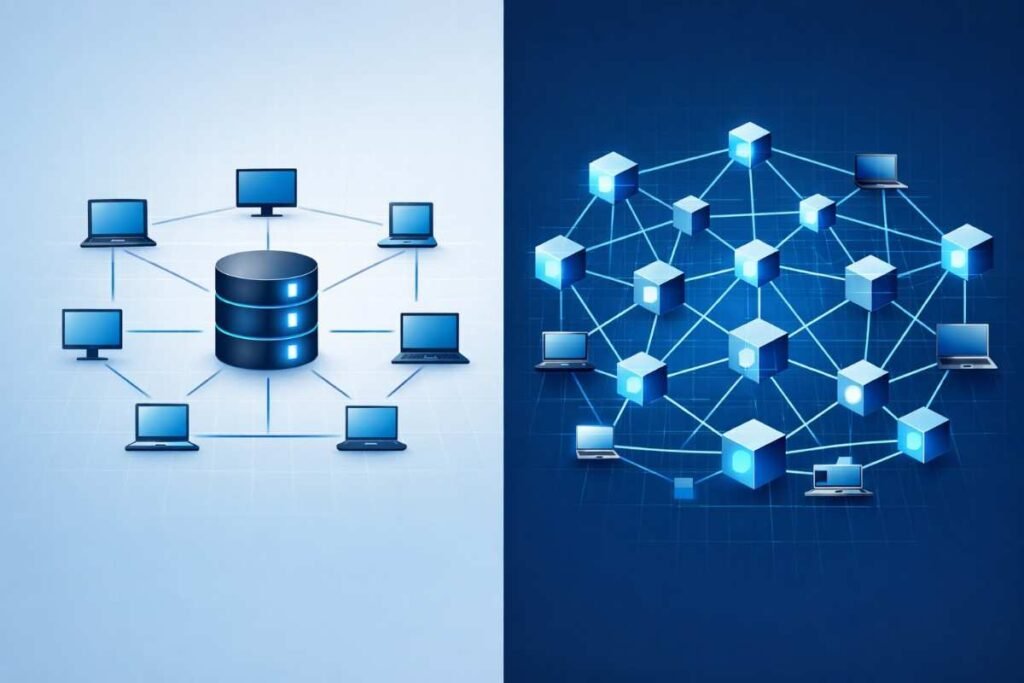

At its core, Blockchain is a system for recording information in a way that makes it difficult or impossible to change, hack, or manipulate. It allows data to be stored across a network of computers instead of a single centralized server. This simple idea has reshaped industries ranging from finance and supply chains to healthcare and governance.

Understanding Blockchain is important not only for developers or investors but also for businesses, policymakers, and everyday users who interact with digital systems daily. This guide explains Blockchain in a clear and practical way, focusing on how it works, why it matters, and where it is being used.

How Blockchain Works

Blockchain is a distributed digital ledger that records transactions in a series of blocks linked together in chronological order. Each block contains a list of transactions, a timestamp, and a cryptographic reference to the previous block. Once a block is added to the chain, its data cannot be easily altered.

To understand how Blockchain functions, it helps to break the process into simple steps.

First, a transaction is initiated. This could be a financial transfer, a data update, or any digital action that needs verification. The transaction is broadcast to a network of computers known as nodes.

Second, the network validates the transaction using consensus mechanisms. These mechanisms ensure that all participants agree on the validity of the transaction before it is recorded.

Third, verified transactions are grouped into a block. This block is then added to the existing chain of blocks. Each block is secured using cryptographic techniques, making it extremely difficult to modify past records.

Finally, the updated ledger is distributed across the network. Every node has a copy of the Blockchain, ensuring transparency and resilience.

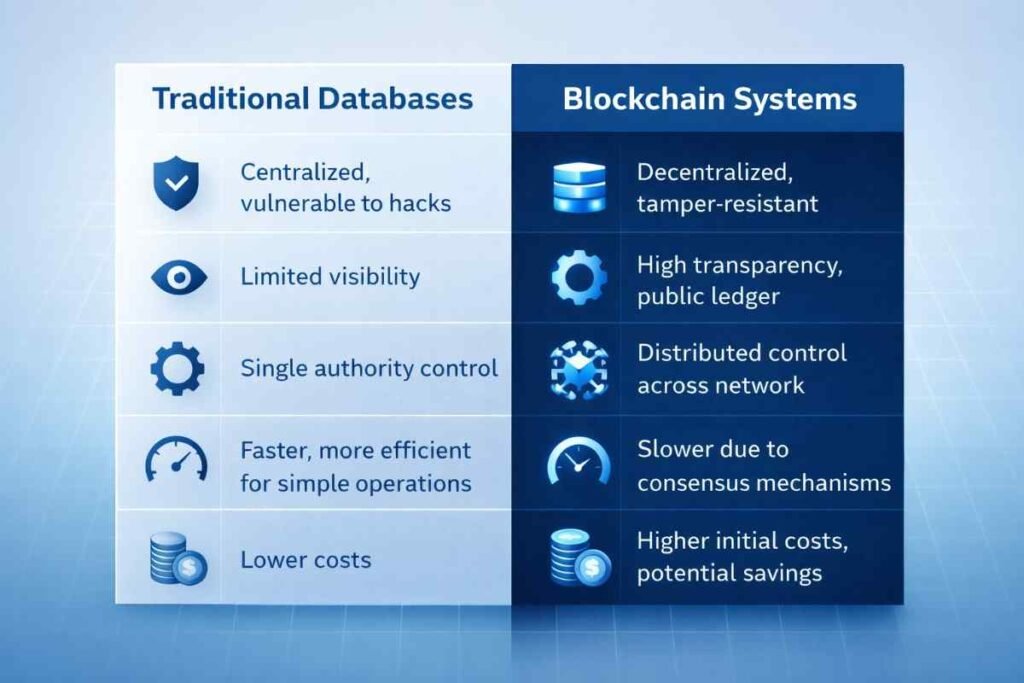

This decentralized structure is what makes Blockchain fundamentally different from traditional databases. Instead of relying on a single authority, trust is distributed across the network.

Key Components of Blockchain

Blockchain systems rely on several core elements that work together to ensure security and reliability.

Blocks:

Each block stores transaction data, a timestamp, and a cryptographic hash of the previous block.

Nodes:

Nodes are computers that maintain and verify the Blockchain. They store copies of the ledger and participate in validation.

Consensus Mechanisms:

These are rules that determine how nodes agree on the validity of transactions. Common methods include Proof of Work and Proof of Stake.

Cryptography:

Cryptographic hashing ensures that data inside blocks remains secure and tamper-resistant.

Distributed Ledger:

Instead of a single central database, the ledger is shared across the network.

Together, these components create a system that is transparent, secure, and resistant to manipulation.

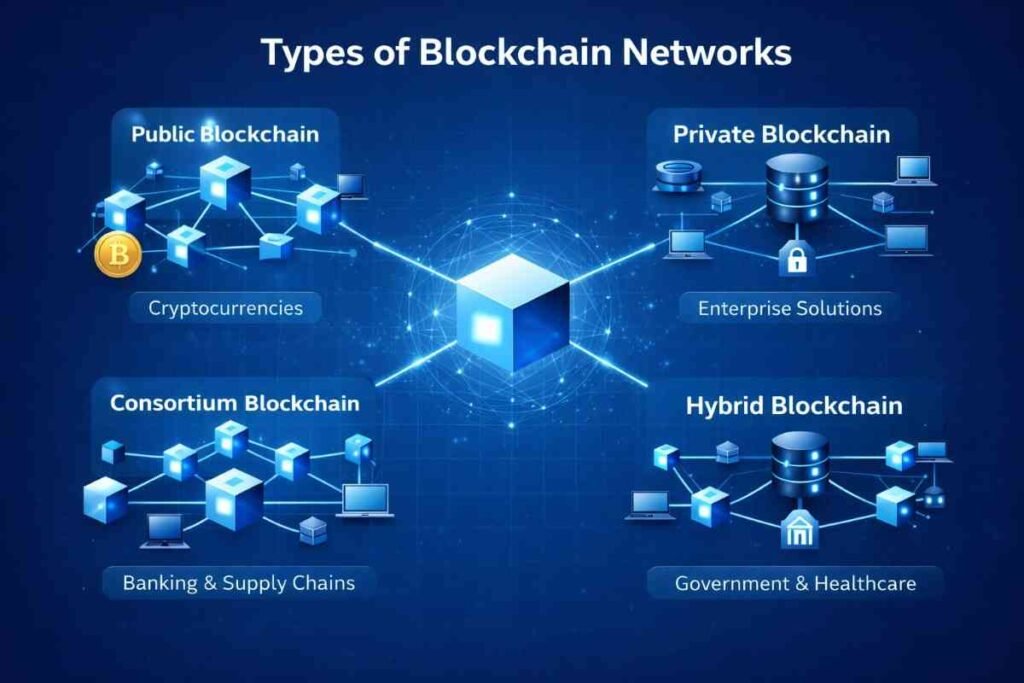

Types of Blockchain Networks

Blockchain networks can be categorized based on access and control.

Public Blockchain:

Open to anyone. Examples include Bitcoin and Ethereum. Anyone can participate, validate transactions, and view data.

Private Blockchain:

Controlled by a single organization. Access is restricted to authorized participants. Common in enterprises.

Consortium Blockchain:

Managed by a group of organizations rather than a single entity. Often used in banking and supply chain industries.

Hybrid Blockchain:

Combines features of public and private Blockchains, allowing selective transparency.

Each type serves different use cases depending on security requirements, scalability, and governance.

Why Blockchain Matters

Blockchain is more than a technological trend. It represents a shift in how trust and data are managed in digital systems.

Decentralization:

Traditional systems rely on central authorities such as banks or governments. Blockchain distributes control across a network, reducing dependency on intermediaries.

Transparency:

Transactions recorded on a Blockchain are visible to participants, increasing accountability.

Security:

Cryptographic techniques and distributed storage make Blockchain highly resistant to hacking and fraud.

Immutability:

Once data is recorded, it cannot be easily changed. This feature is crucial for maintaining data integrity.

Efficiency:

Blockchain can reduce transaction costs and processing times by eliminating intermediaries.

These advantages explain why Blockchain is being adopted across multiple industries.

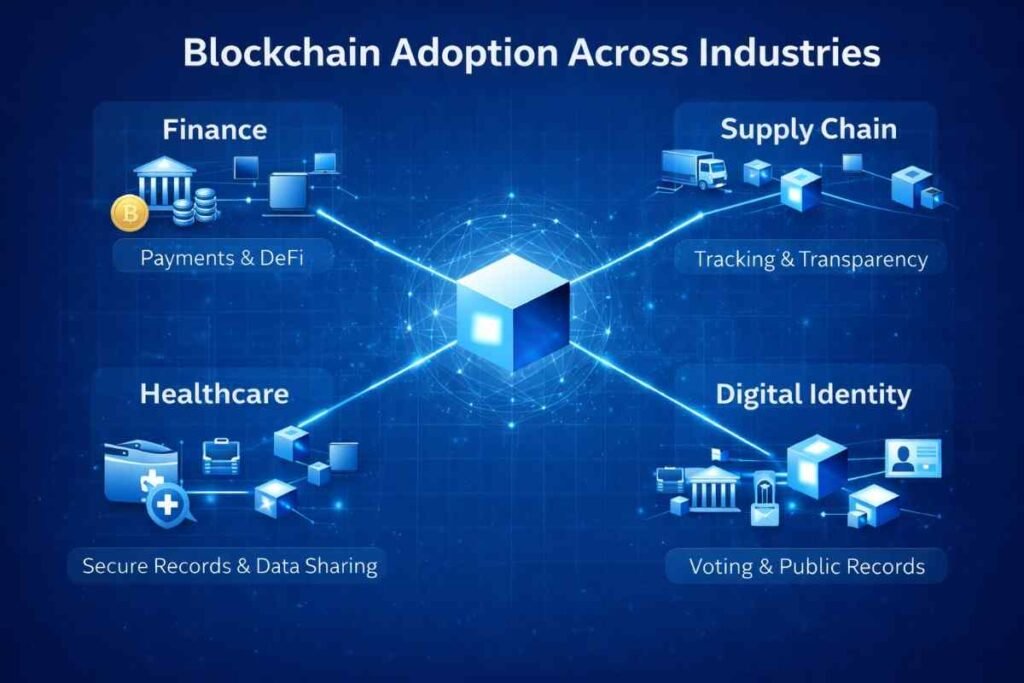

Real-World Applications of Blockchain

Blockchain technology is being used far beyond cryptocurrencies. Its applications continue to expand as organizations explore decentralized systems.

Financial Services:

Blockchain enables faster and cheaper cross-border payments. It also supports decentralized finance platforms that operate without traditional banks.

Supply Chain Management:

Companies use Blockchain to track goods from origin to destination. This improves transparency and reduces fraud.

Healthcare:

Blockchain helps secure patient records and enables safe data sharing between healthcare providers.

Digital Identity:

Blockchain-based identity systems allow individuals to control their personal data and reduce identity theft.

Smart Contracts:

These are self-executing agreements coded on a Blockchain. They automate processes such as insurance claims and real estate transactions.

Government and Public Services:

Some governments use Blockchain for voting systems, land registries, and public record management.

Blockchain and Cryptocurrency

Blockchain is often associated with cryptocurrencies, but the two are not the same.

Cryptocurrency is a digital asset that uses Blockchain as its underlying technology. Bitcoin was the first major cryptocurrency to demonstrate how Blockchain could enable peer-to-peer transactions without intermediaries.

Today, thousands of cryptocurrencies operate on various Blockchain networks. However, Blockchain itself can exist without cryptocurrencies. Many enterprise solutions use Blockchain purely for data management and automation.

Understanding this distinction is important for grasping the broader impact of Blockchain technology.

Benefits and Limitations of Blockchain

Like any technology, Blockchain has strengths and challenges.

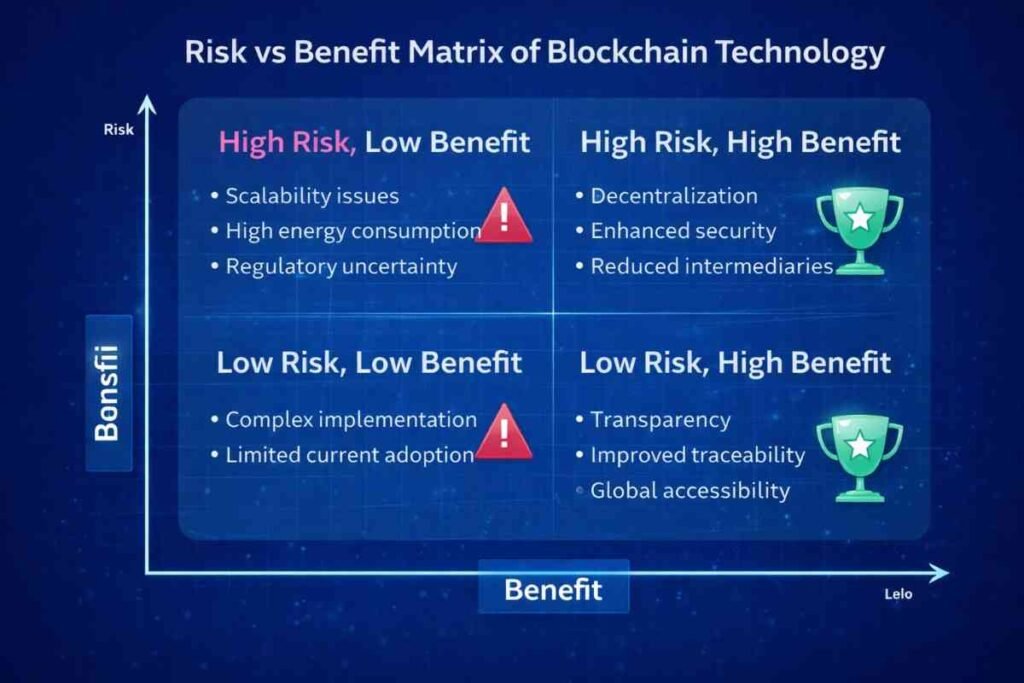

Benefits:

- Enhanced security and transparency

- Reduced reliance on intermediaries

- Improved traceability of data

- Automation through smart contracts

- Global accessibility

Limitations:

- Scalability issues in some networks

- High energy consumption in certain consensus mechanisms

- Regulatory uncertainty

- Complexity of implementation

- Limited adoption in some sectors

These challenges are driving ongoing research and innovation in Blockchain systems.

Blockchain in Business and Enterprise

Businesses are increasingly exploring Blockchain to improve operational efficiency and trust.

Large corporations use Blockchain to streamline supply chains, verify authenticity of products, and manage contracts. Financial institutions experiment with Blockchain-based settlement systems to reduce costs and delays.

Startups leverage Blockchain to create decentralized platforms that challenge traditional business models. Meanwhile, governments evaluate Blockchain for secure digital infrastructure.

The enterprise adoption of Blockchain suggests that the technology is moving beyond experimentation toward real-world implementation.

Future of Blockchain

The future of Blockchain depends on technological advancements, regulatory frameworks, and user adoption.

Scalability solutions such as layer-two networks aim to increase transaction speed and reduce costs. Interoperability projects focus on connecting different Blockchain networks. Regulatory clarity could encourage institutional adoption.

In the long term, Blockchain could become a foundational layer of digital infrastructure, similar to how the internet transformed communication and commerce.

While predictions vary, most experts agree that Blockchain will continue to play a significant role in shaping the digital economy.

Conclusion

Blockchain is a transformative technology that changes how information is stored, verified, and shared. By decentralizing control, enhancing transparency, and strengthening security, it offers an alternative to traditional centralized systems.

From financial services to healthcare and governance, Blockchain is reshaping industries and redefining digital trust. Although challenges remain, ongoing innovation and adoption suggest that Blockchain will remain a key pillar of the digital future.

For individuals and organizations alike, understanding Blockchain is no longer optional. It is becoming essential for navigating the evolving digital landscape.

Read Also: What Is Cryptocurrency? Ultimate Guide for Beginners and Investors